{kind=link}

Today, a trip to the bank is something most people barely think about. A few taps on a screen can move money across the world, while a visit to an ATM or teller might take only minutes. Mortgages can be renewed online, bills can be paid instantly, and savings accounts can be opened with little more than a piece of identification.

But in Bytown’s earliest days, banking was chaotic, unpredictable, and often risky.

Long before Ottawa had its first bank branch, residents relied on a confusing mix of foreign coins, handwritten letters of credit, merchant-issued currency, and distant banking agents. There was no standardized Canadian currency, little regulation, and constant uncertainty over whether the money in circulation was actually worth what it claimed to be.

In many ways, early Bytown operated like a frontier settlement of the financial “wild west.”

An actual bank branch would not arrive for some 16 years after Bytown’s founding. Rather, some of the earliest Canadian banks sent agents to Bytown to help handle certain types of transactions.

Bytown was still very small, limiting the need for a full bank branch. Additionally, there were legal limitations on which banks could open where – for instance, the Bank of Montreal, which was founded in Montreal in 1817 (originally as “the Montreal Bank”), could not open a branch in Bytown as it had its headquarters in Lower Canada even though one of its directors was John Redpath, a key contractor in the construction of the Rideau Canal.

On top of this, there was great instability in the banking and financial world at the time. Canada did not yet have a common currency, and banks, as they were just starting up, might issue their own notes and bills, but these were unproven and accepting them was high risk. Silver might have been used more widely as currency had there not been a major coin shortage in the early 19th century.

As a result, trade relied on a mix of foreign and colonial money. Spanish silver dollars (aka pieces of eight) from Spain, Portugal, and Mexico were trusted worldwide. They were commonly found in North America and, for a long time, were considered a standard. Colonies in Canada used a currency rating known as Halifax Currency (where one Spanish dollar was worth 5 shillings). Lesser-used but still prevalent were British, French and American coins, while the first paper money began to appear through issuance from the British military and private merchants.

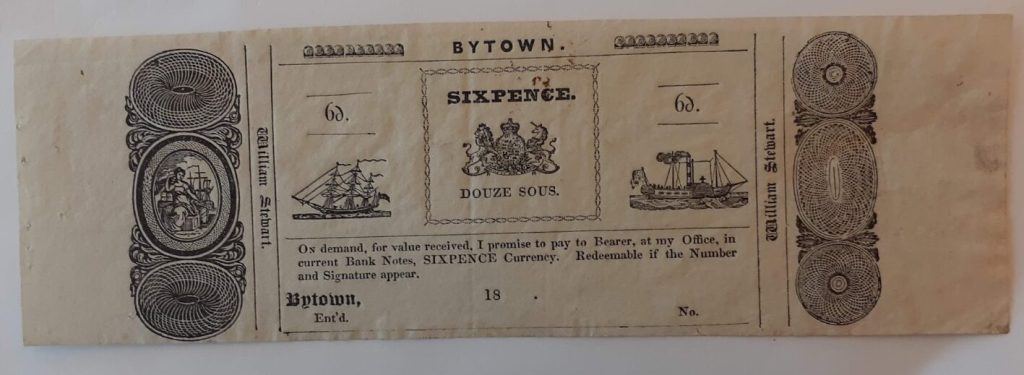

One such example that survives is a sixpence “merchants’ script” from shopkeeper and tavern owner William Stewart of Bytown, from approximately 1836 (around which time Stewart’s younger brother Roderick Stewart had become the first settler in what is now Wellington Village, establishing a farm along Richmond Road).

Agents would also issue letters of credit, which were accepted by the general public as good as cash if the letter-holder could convince the recipient to accept them.

Essentially, it was a free-for-all whereby merchants and citizens used a mix of currencies to borrow and pay. There was almost always a risk that the currency would retain its value or lose it entirely if the note, letter, or bill proved to be counterfeit, the bank went out of business, or the issuer simply disappeared.

A risky business

Banks began operating in more populated areas of Ontario and sent agents to Bytown to conduct business.

Before the construction of the Canal commencing in 1826, there were no records of bank agents in town. Still, the building of the Canal meant that employment and the local economy would soon be booming – Bytown would see its population rise from only a few dozen residents to nearly 2,000 by the time the Canal was completed.

However, early banks offered only limited services. In the early 1800s, there were no savings accounts, no mortgages, no personal cheques. The banks focused almost exclusively on commercial clients and international trade.

According to historian James Powell, issuing currency was a big focus of early banks.

“Banks in those days, their big business was the currency issue. They could issue notes equivalent to their capital reserves. So it was very profitable to get your notes out there. Agents in Bytown were doing their best to get the parent bank’s notes in circulation in Bytown, as it was even better to have them circulating far away from where the bank of issue was located, because it was less likely for those notes to come back and be redeemed for gold.”

This also allowed fraudsters to take advantage of the situation. As Powell continues, “It was a time when some fraudulent banks would do that. They would set up shop somewhere remote, print off currency, and have it circulated far away from where they were in the hopes that not much would come back for redemption.”

Those holding the notes often faced uncertainty about what they held. “You hoped it was good”, Powell says. “Like a hot potato. If you were buying something from someone else, you would use those notes and hope they’d accept them. If they did, it was no longer your problem; it was someone else’s.”

He also notes that the further away a currency was used, the less value it might have. “If you’re in Bytown, and you got a note from a bank in Toronto, let’s say it’s a 10-dollar bill, you might only get 8 dollars value for it. Bank notes of different banks were discounted depending on how far they were from the place where they were exchanged for gold, taking into account transportation costs, as well as how legitimate or not the banks might be. If you’re offered 8 dollars value for your bill, it’s up to you to take it or leave it, basically.”

Fortunately for the workers on the canal, they were typically paid in hard cash, largely in Mexican silver dollars, and the workers simply spent as they went. Making things even more tricky was the fact that most commerce in Bytown at the time was “company stores” operated by the British government and later by the lumber barons. Essentially, the workers were giving back the money their employers had paid them. Or they simply had deductions made from their wages in exchange for necessities such as food, clothing, and tools.

Many Canal contractors were paid in Mexican coins. It was reported that Redpath and Thomas Mackay had to “cart home” their part of the profits, with coins packed in barrels, forwarded by the Ordnance Department from Quebec, and delivered by wagon and wheelbarrow into the vaults of the Bank of Montreal. The British Ordnance Department at the time were flush with coins seized from ships captured by the Royal Navy.

The first bankers of Bytown

Who was the first banker to arrive in Bytown? A definite answer appears to have been lost to time.

Early records indicate that some banking was conducted by George and Robert Lang, who were involved in the timber trade, and who made collections for the Commercial Bank of the Midland District (headquartered in Kingston) and occasionally issued letters of credit against their own accounts. Captain George W. Baker, a captain in the Royal Artillery, became Bytown’s second postmaster in 1834, but was also an agent for the Bank of Upper Canada, which was tied closely to the governing oligarchy (aka the Family Compact).

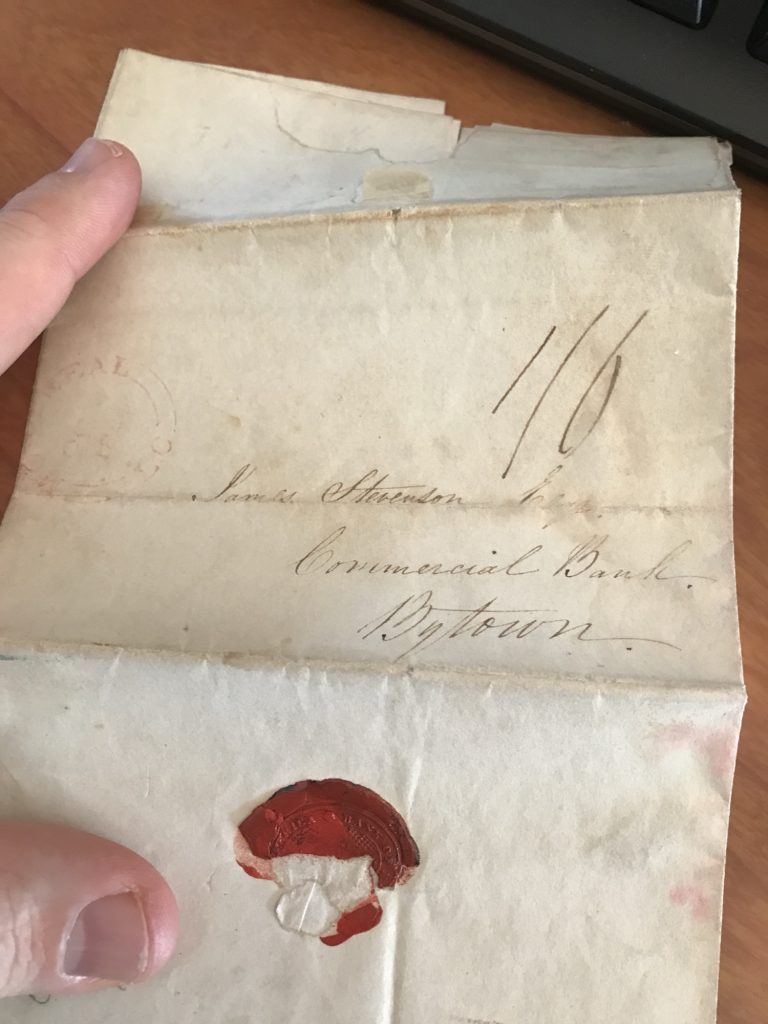

James Stevenson Sr. was appointed agent and cashier of the Commercial Bank in Bytown in the late 1830s, a role he held alongside his position as Crown Timber Agent (issuing timber limits and collecting slide dues), a post he held from 1836 to 1851. An 1842 letter addressed to him in his Bytown banking role remains one of the earliest documents in our city’s banking history.

His son James Stevenson Jr., meanwhile, had been working in the Crown Lands office in Quebec City (helping manage settlement and development of public lands as Canada began to grow) from 1839 to 1842, where he too was in regular contact with that city’s lumber merchants and bankers.

Meanwhile, Bytown had emerged as a key center in the lumber trade, especially with the recently completed timber slides around the Chaudiere Falls. “This essential public improvement had become a valuable source of provincial revenue, and it was for this reason, no doubt, that the Bank decided to open a branch there,” noted the Bank of Montreal in its 1966 self-published history.

As branch restrictions disappeared when Upper and Lower Canada united into the Province of Canada in 1842, the Bank of Montreal decided to open Bytown’s first bank branch here in a small office inside a Wellington Street hotel that same year, 1842. James Jr. was selected as its manager.

The Bank of Montreal, when publishing its history in 1966, commissioned an illustration of this first Bytown bank. Artist John Little painted the 1842 scene of James Jr. standing on the plank sidewalk on Wellington, speaking with two logger customers.

The future Parliament Hill was still just vacant land, and there was practically lawlessness in Bytown, with street fights and gang battles common. Wellington Street itself was still just a muddy footpath with a gate at each end.

The tasks in running the bank branch were not onerous, but as the other bank agents had limited powers, Stevenson was the only agent able to cash drafts. Thus, he had no choice but to be available at all hours.

“Roistering lumber-jacks and rivermen poured into Bytown in the spring after spending long, monotonous months in the woods. Those still ambulatory after a night of conviviality, and planning to leave with their rafts at the first light of dawn, often wanted drafts or cheques cashed, and they beat upon the agent’s door without regard for the hour until they were served,” recounted the Bank of Montreal in their history.

In one well-reported instance, Stevenson was awoken in the middle of the night and, still drowsy, handed a man a package containing one thousand four-dollar bills, rather than one-dollar bills. Luckily, he noticed his mistake before it was too late.

There was no vault in the building, and no other security available. Thus, Stevenson would carry the money and key paperwork to and from the bank each day in tin cashboxes. “These were kept under the agents’ beds at night, so that they could be reached easily in case of fire,” reported the Citizen in a later history.

Ottawa’s financial district begins to emerge

In 1844, the Bank of Montreal moved into a limestone building, the Royal Exchange Hotel on Wellington Street (now the site of the Bank of Canada), renovated it, and remained there until 1873.

Meanwhile, the Bank of British North America opened a branch in Brockville in 1843 and recruited James Jr. to manage it. So, his father, James Sr., was appointed to take over the Bank of Montreal branch in Bytown.

By 1847, Bytown had four banks operating: The Bank of Montreal, the Commercial Bank, the Bank of Upper Canada (agent Thomas J. Leggatt), and the Bank of British North America (agent John McKinnon).

A fifth bank, the Quebec Bank (with agent H. V. Noel), opened in 1848. The Quebec Bank became a leader in the banking industry at the time by catering to the needs of the transatlantic timber market. Bytown played a key role as the centre of the Ottawa Valley timber trade. The port of Quebec City was the major global staging centre where huge log rafts from areas like Bytown would arrive and be loaded onto ships headed to Europe.

The Quebec Bank was able to provide direct banking services to exporters, ship owners and timber brokers. They were one of the few institutions in Canada capable of providing the extensive liquidity and credit required to sustain the major lumber barons. The Bytown branch was reportedly its most profitable branch, located in a stone building on Metcalfe Street.

Soon, Bytown was chosen as Canada’s capital, and major public works projects began to build the infrastructure befitting of a capital city. The population of Bytown rose to approximately 10,000 by the time it was granted city status and renamed Ottawa in 1855.

By 1861, the Commercial Bank had closed its Ottawa office. Still, the remaining four banks remained, with all of their offices located on Wellington Street, “gathered near each other for safety against fire and thieves,” noted the Ottawa Citizen.

Soon, the Royal Bank of Canada would absorb the Quebec Bank, and the Bank of Upper Canada collapsed in 1866 after suffering major losses from careless land and railway speculation and from issuing too many loans on poor security. The aftermath saw the Canadian government overhaul the national banking system.

The Bank of British North America would carry on until it was absorbed by the Bank of Montreal in 1918. The Bank of Montreal maintained a dominant position in Ottawa’s financial life during the 19th and 20th centuries, including, and especially, its role as the official banker for the Dominion government.